Featured

Table of Contents

Browsing Credit Difficulties in Garland Debt Management Program

Economic shifts in 2026 have altered how homes manage their month-to-month obligations. With interest rates holding at levels that challenge even disciplined savers, the traditional methods of surviving are showing less effective. Many residents in Garland Debt Management Program are looking at their financial declarations and seeing a bigger portion of their payments approaching interest instead of the primary balance. This shift has resulted in a restored interest in structured financial obligation management programs offered by not-for-profit firms.

The primary hurdle in 2026 remains the cost of unsecured credit. Charge card business have actually changed their danger designs, often resulting in greater interest rate for customers who carry balances from month to month. For those residing in your local area, these costs can rapidly outmatch wage growth, creating a cycle where the total balance remains stagnant despite routine payments. Specialists concentrating on Financial Wellness recommend that intervention is most effective when started before missed payments begin to harm credit rating.

Comparing Consolidation Loans and Management Programs in 2026

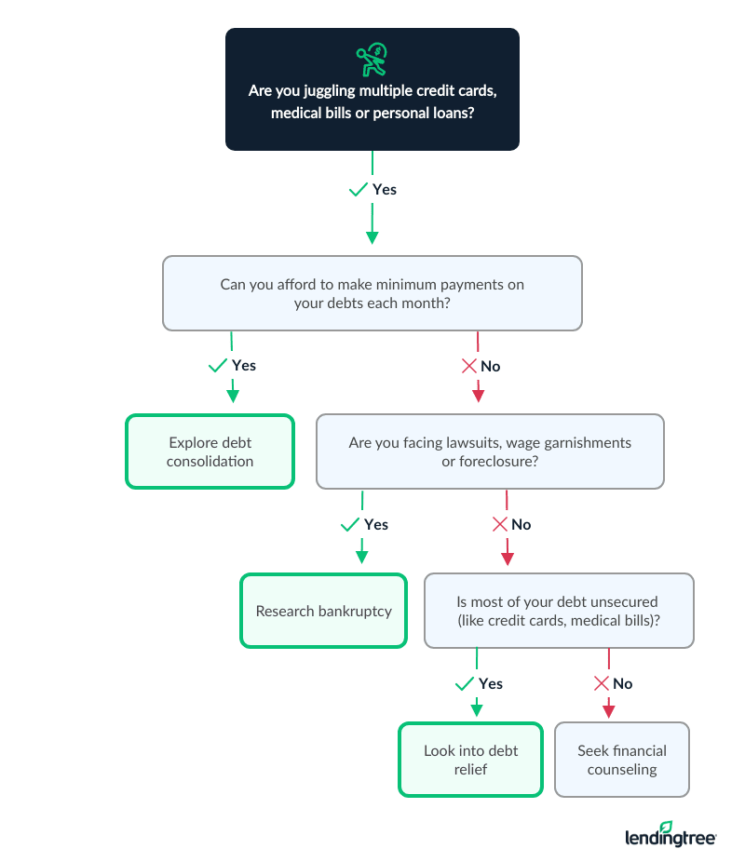

Monetary strategies in 2026 typically include choosing between 2 distinct courses: financial obligation combination loans and debt management strategies. A combination loan involves taking out a new, big loan to pay off several smaller debts. This technique depends greatly on a person's credit report and the accessibility of beneficial terms from private lenders. In the current market, nevertheless, protecting a low-interest individual loan has actually ended up being significantly tough for those who are currently bring significant financial obligation loads.

Personal Financial Wellness Programs offers a structured option to high-interest loans by working within the existing lender relationships. Unlike a loan, a debt management strategy does not involve borrowing more money. Instead, it is a negotiated arrangement helped with by a nonprofit credit therapy firm. These agencies work with lenders to lower rate of interest and waive specific fees, enabling the consumer to settle the full principal over a set duration, generally three to five years. For lots of in the surrounding area, this method offers a clear timeline for reaching zero balance without the need for a brand-new line of credit.

The distinction is considerable for long-lasting monetary health. While a loan simply moves financial obligation from one place to another, a management plan focuses on methodical payment and behavioral modification. Counseling sessions related to these programs frequently include spending plan reviews that help participants identify where their money goes each month. This educational component is a hallmark of the 501(c)(3) not-for-profit design, which prioritizes consumer stability over profit margins.

The Mechanics of Interest Rate Negotiation in your local area

One of the most efficient tools offered to customers in 2026 is the ability of credit therapy companies to negotiate directly with significant banks and card companies. These negotiations are not about opting for less than what is owed-- a procedure that typically ruins credit-- but about making the repayment terms manageable. By decreasing a 24 percent interest rate to 8 or 10 percent, a program can shave years off the repayment period and conserve the customer thousands of dollars.

People frequently search for Financial Wellness in Garland TX when handling several lender accounts ends up being a logistical problem. A management strategy simplifies this by combining numerous regular monthly bills into a single payment. The not-for-profit agency then distributes that payment to the different creditors according to the worked out terms. This structure lowers the probability of late charges and ensures that every account stays in good standing. In Garland Debt Management Program, this simplification is often the primary step toward restoring control over a household spending plan.

Financial institutions are often ready to take part in these programs since they prefer getting routine, complete payments over the risk of an account entering into default or personal bankruptcy. By 2026, numerous banks have structured their cooperation with Department of Justice-approved agencies to help with these strategies more effectively. This cooperation benefits the customer through reduced tension and a predictable path forward.

Strategic Financial Obligation Repayment in across the country

Housing and credit are deeply linked in 2026. Many households in various regions discover that their ability to certify for a home loan or preserve their present home depends upon their debt-to-income ratio. High credit card balances can inflate this ratio, making it hard to access favorable housing terms. Nonprofit companies that provide HUD-approved real estate counseling frequently incorporate financial obligation management as part of a bigger method to support a household's living scenario.

The effect on credit report is another factor to think about. While a debt management plan requires closing the accounts consisted of in the program, the consistent on-time payments usually assist reconstruct a credit profile with time. Unlike financial obligation settlement, which includes stopping payments and letting accounts go to collections, a management strategy shows a dedication to honoring the original financial obligation. In the eyes of future lending institutions, this difference is important.

- Decreased rate of interest on charge card accounts.

- Waived late costs and over-limit charges.

- Single monthly payment for several unsecured debts.

- Expert assistance from certified credit therapists.

- Education on budgeting and monetary literacy.

As 2026 advances, the role of monetary literacy has actually moved from a luxury to a requirement. Comprehending the difference in between protected and unsecured debt, the impact of compounding interest, and the legal securities available to customers is essential. Not-for-profit agencies serve as a resource for this information, providing services that go beyond mere financial obligation repayment. They provide the tools required to avoid future cycles of debt by mentor participants how to develop emergency funds and handle capital without depending on high-interest credit.

Long-Term Stability Through Structured Preparation

The decision to enter a debt management program is often a turning point for families in Garland Debt Management Program. It marks a shift from reactive spending to proactive planning. While the program needs discipline-- specifically the dedication to stop using charge card while the plan is active-- the outcome is a debt-free status that supplies a structure for future conserving and financial investment.

Financial advisors in 2026 highlight that there is no one-size-fits-all solution, however for those with significant unsecured financial obligation and a stable income, the structured approach of a not-for-profit strategy is often the most sustainable choice. It prevents the high charges of for-profit settlement business and the long-term credit damage of insolvency. Instead, it uses a middle path that balances the requirements of the customer with the requirements of the financial institution.

Success in these programs depends on transparency and consistent communication with the counselor. By examining the budget quarterly and making changes as living costs change in your region, individuals can stay on track even when unanticipated expenditures emerge. The goal is not just to settle what is owed, however to exit the program with a various viewpoint on how to utilize credit in a way that supports, instead of hinders, monetary progress.

Ultimately, the role of financial obligation management in a 2026 monetary strategy is to provide a clear exit from high-interest responsibilities. By focusing on primary decrease and interest settlement, these strategies permit locals in Garland Debt Management Program to reclaim their income and concentrate on their long-lasting goals. Whether the goal is buying a home, conserving for retirement, or simply lowering daily stress, a structured payment plan provides the framework essential to attain those ends.

{kind=link}

Latest Posts

Top Tips for Handling Credit Card Debt in 2026

Why Your Credit Report Looks Different in Your City

Discovering Inexpensive Consolidation Solutions in Your Local Area